In this article, VTDigger assesses the impact of the Affordable Care Act in the six New England states. Our analysis is based on spending and enrollment data for federally qualified health plans.

The landmark federal health care law recently marked its fourth anniversary, and online insurance marketplaces were launched six months ago.

Federal funding for implementing the Affordable Care Act was made available to states through implementation grants. The grants were earmarked for states, which are billing the feds for expenses as the money is spent.

Significantly more cash was made available to states that chose to build their own online insurance marketplaces, known as exchanges, than for states that opted to use the federally built exchange.

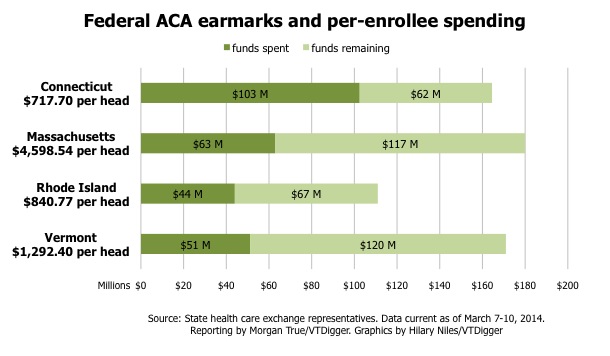

Four of the 14 states plus the District of Columbia that chose to build their own exchanges are in New England. Vermont, Connecticut, Rhode Island and Massachusetts all received earmarks of up to $100 million.

The above chart shows a snapshot of how much each state spent the federal money. The figures were collected from March 7 to March 10. The per-head spending figure reflects how many people had enrolled in health coverage through the state’s online marketplace at that time.

The return on spending varies widely, with Connecticut’s exchange being touted as a national model. Massachusetts is among the states with the least to show for its efforts.

Despite spending $63 million of its $180 million earmark, 62,000 Bay State residents had temporary coverage, as of early March, according to a spokesman for Massachusetts Health Connector, the state’s exchange.

The spokesman said $69 million of Massachusetts’ exchange funding was slated for the Connector website, but only $15 million of those funds had been spent as of early March. Since the figures were collected, Massachusetts dropped the tech firm responsible for the website, CGI — the same company that is responsible for Vermont’s exchange sites.

Of Vermont’s $171 million earmark, $54 million was set aside for the initial creation and launch of the Vermont Health Connect website. Vermont’s contract with CGI is worth $84 million; $30 million of that sum is for ongoing maintenance and operation of the site during the first two years of operation. The maintenance and operational money will be built into the state budget over the next three years.

The latest figures show Vermont has paid CGI more than $19 million for a website that still lacks significant functionality.

Rhode Island has also struggled to get its exchange functioning properly, and lawmakers in the Ocean State were at one point pushing to scrap their website and go with the federal healthcare.gov website instead.

Enrollment figures used to calculate the per-head spending figure include people that sought coverage through the exchanges and discovered they qualified for Medicaid as part of that program’s expansion through the Affordable Care Act.

The figures do not include populations in Vermont and Massachusetts that were automatically transitioned from state-subsidized health insurance programs to Medicaid. In Vermont, roughly 35,000 people formerly on VHAP or Catamount are now on Medicaid. The numbers also do not include people enrolled in exchange-based plans from the small group market.

Vermont is the only state to require businesses with 50 or fewer employees to purchase coverage through its exchange, but small businesses have been unable to use the Vermont Health Connect website. More than 30,000 Vermonters have coverage because the two private insurers offering plans through the exchange picked up the slack for the state and enrolled small businesses directly.

Vermont’s insurers on the exchange have suggested that expenses related to direct enrollment might be built back into their premium rates in 2015.

New Hampshire, Maine and 34 other states went for the federal option. New Hampshire has spent more than $4 million of $8.6 million earmarked for implementation of the Affordable Care Act. Republican lawmakers in the state have blocked appropriations of additional federal funds, according to a spokesman for Democratic Gov. Maggie Hassan.

Maine has spent $4.4 million; a spokeswoman for MaineCare was not able to provide a figure for the state’s available earmark. Tens of thousands in state money is included in the total.

Comparing spending among the New England states that built their own exchanges against those who used the federal exchange website is an apples to oranges juxtaposition. Maine and New Hampshire rely on healthcare.gov, which the feds have spent hundreds of millions to build and fix after a rocky rollout.

In addition, the New England states that built their own exchanges accepted the federal Medicaid expansion, and, as a result, tens of thousands of residents in each state are newly enrolled in the program.

Maine’s Republican Gov. Paul LePage is vehemently opposed to the expansion, and Democrats there have waged an unsuccessful campaign to do so in the face of his opposition. The Republican-controlled New Hampshire Senate recently approved a partial Medicaid expansion, which is likely to sail through the Democrat-dominated House.

The federal government is covering the entire cost of the Medicaid expansion in its first three years, and will cover 93 percent of those costs between 2014 and 2022, according to the nonpartisan Center on Budget and Policy Priorities, a D.C.-based think tank.

In a recent segment on “Fox News Sunday,” Gov. Peter Shumlin sparred with Republican Gov. Scott Walker of Wisconsin over the decision to accept or reject the expansion.

Shumlin said Republican governors who rejected the expansion are denying tens of thousands, and in some cases hundreds of thousands, of residents access to affordable health coverage in order to make a political point.

Walker defended his rejection of the Medicaid expansion. He said he was shielding his state from risk, because Congress, with the blessing of a new administration, could enact entitlement reform in the future that would rescind funding for the expansion and leave states that accepted it on the hook for the cost.

This chart shows the percentage of people who signed up for health coverage through the exchanges in each state that will receive a subsidy to reduce the cost of that coverage.

The data comes from the U.S. Department of Health and Human Services and was collected through the end of January. The feds began publishing monthly reports in February with figures from the previous month.

The report released in March provides far less detail, and does not include state-by-state percentages for the number of enrollees qualifying for subsidies. However, figures from mid-March presented to lawmakers by Mark Larson, commissioner of the Department of Vermont Health Access, show that the percentage of people qualifying for subsidies in Vermont has not changed appreciably since the January figures collected by HHS.

Nationally, 83 percent of people are qualifying for subsidies compared to just 54 percent in Vermont. The next lowest New England state is Maine, which has the most similar population and age demographics to Vermont, at 72 percent.

A lower percentage of Vermonters are qualifying for subsidies, according to Larson, because Vermont Health Connect is the only place individuals can purchase insurance, while people in other states can go elsewhere to purchase ACA-compliant plans.

“Basically, our denominator, or pool of people using the exchange, is relatively larger than in other states,” said Larson in an email. “It’s important to note that the majority of Vermonters who are using Vermont Health Connect to get an individual/family plan are enrolling in Medicaid. While Medicaid is very low cost, it is not included in the measure of who is getting subsidies.”

However, the same is true in other states that accepted the Medicaid expansion.

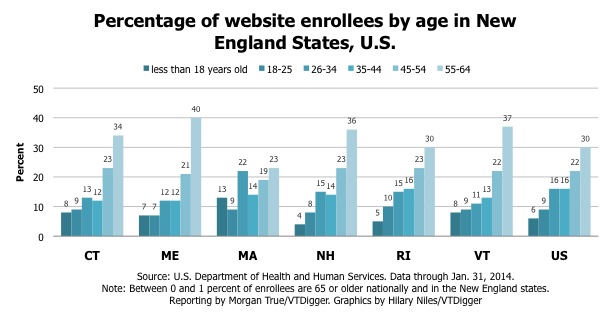

This chart shows the age-demographics of exchange enrollment in the New England states and nationally. It was made using the same, more detailed data HHS presented in its first report with data through the end of January.

There has been much discussion and speculation nationally about whether the insurance risk pools created via the exchange marketplaces could sign up enough so-called “young invincibles,” or people aged 18-34, who believe themselves healthy and therefore disinclined to pay for health insurance.

Nationwide the percentage of 18- to 34-year-olds enrolling in coverage through the exchanges is 25 percent. In Vermont its 20 percent, lower than any of the New England states except Maine, which brings up the rear at 19 percent.

Many argue the viability of the individual health insurance markets on the exchange is predicated on enough young people purchasing insurance to offset older less healthy enrollees, who are more likely to seek medical care.

However, that narrative doesn’t hold in Vermont, according to Larson.

“Frankly Vermont is different in this conversation,” he told lawmakers, when asked if he was concerned about the demographics of the state’s enrollees. “Vermont Health Connect is the individual and small group market. If we have transitioned the market that was in the past, the Vermont Health Connect market is as viable as last year’s market.”

To ensure Vermont Health Connect had a viable individual market, Vermont made a policy decision that individual plans would only be available through the exchange.

If the state had not, it’s possible Vermont’s aging population would’ve exposed insurers offering coverage through the exchange to unacceptable levels of risk.

This article was updated at 9:49 a.m. on March 31, 2014.