In 2014, more Vermonters than ever will be eligible for health insurance subsidies.

Thousands of Vermonters earning up to 400 percent of the federal poverty level will be eligible for federal and state premium subsidies as of Jan. 1.

At the end of the year, federal premium subsidies will be reconciled based on Vermonters’ actual incomes. Vermonters who experience an income increase could owe the federal government taxes. Residents who see their income drop could be eligible for a rebate.

Federal and state cost-sharing subsidies are available to Vermonters earning up to 300 percent of the federal poverty level. Cost-sharing subsidies reduce out-of-pocket costs by capping liability limits, deductibles and copayments.

Neither the premium nor the cost-sharing subsidies are available to workers who are offered health insurance from their employers, unless the employer contribution is deemed unaffordable.

For more on affordable and unaffordable contributions click here.

Premium and cost-sharing subsidies differ. Cost-sharing subsidies can only be used with silver level plans, while premium subsidies can be used for any plan.

Vermont’s health insurance market, called Vermont Health Connect, offers four general categories of coverage.

The plans range from bronze plans, with the lowest premiums and the lowest level of coverage, to the mid-level silver and gold plans, and finally platinum plans that have the highest premiums and broadest level of coverage. The two state approved insurers — Blue Cross and Blue Shield of Vermont and MVP Health Care — are selling 18 plans that fall in these four general categories.

Employees can still qualify for subsidies even if an employer contributes to an employee’s health savings account. Though this information was verified by the U.S. Treasury, the Shumlin administration warns this policy may be subject to change.

A health savings account can be used to pay out-of-pocket costs with pre-tax dollars, and can only be used with select plans. For more on this type of account and other pre-tax accounts, click here.

While new premium programs are available in 2014, the state-subsidized Catamount and VHAP programs are coming to an end. The programs were extended until March 31 as part of a contingency plan, resulting from Vermont Health Connect’s technical problems.

Some low-income working Vermonters who were enrolled in Catamount and VHAP will see reduced premiums and some will see an increase. To learn more, read here.

Out-of-pocket limits will increase for many Vermonters who are not eligible for Medicaid. The rise in limits is due to a reduction in cost-sharing subsidies, which was prompted by a decision from the federal government and subsequent decisions from the administration and the House Health Care Committee.

About 40,000 new Vermonters are expected to access Medicaid’s free or low-cost coverage in 2014, and the state’s hallmark subsidy program for low-income children, Dr. Dynasaur, will continue.

The subsidy equation and Medicaid

To provide Vermonters with an idea of what subsidies they are eligible for, VTDigger used federal poverty guidelines for this year. The 2014 guidelines will not be released until after Jan. 1.

To determine eligibility for subsidies, incomes are calculated using modified adjusted gross income, which is a person’s total adjusted gross income — line 37 on an IRS 1040 form — and tax-exempt items such as tuition, student loan interest and certain self-employment expenses.

All Vermonters with a modified adjusted gross income of less than 138 percent of the federal poverty level will be eligible for Medicaid. That means Medicaid will cover individuals earning up to $15,860 annually, two-person households earning up to $21,400, and four-person households earning up to $32,500.

On paper, the Medicaid eligibility level only goes up to 133 percent of the federal poverty line, but in practice it will go up to 138 percent because the government is allowing a 5 percent increase.

For more on changes to Medicaid, read here.

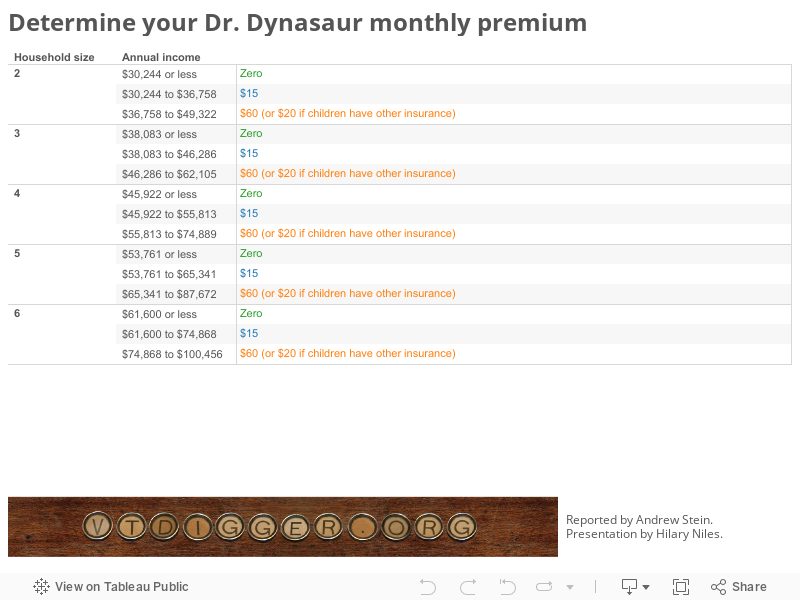

Dr. Dynasaur

Dr. Dynasaur provides lower income children with physical, vision, mental health and dental coverage. It is part of the federal Children’s Health Insurance Programs, known as CHIP. On Jan. 1, Dr. Dynasaur will cover children up to 19 years of age.

To ensure that the new modified adjusted gross income calculation doesn’t prevent children from accessing Dr. Dynasaur benefits, the feds raised eligibility limits.

In 2014, families earning up to 195 percent of the federal poverty level don’t need to pay premiums for their children’s Dr. Dynasaur coverage. Families earning between 195 and 237 percent of the federal poverty level must pay $15 a month for their children to go on Dr. Dynasaur. Parents earning between 237 and 318 percent of the federal poverty level would pay $60 a month for their children to go on Dr. Dynasaur. And parents at this same income level pay $20 a month if their children are covered by another type of health insurance.

The monthly premium for Dr. Dynasaur is a per-family rate, not a per-child rate. That means two families each earning 200 percent of the federal poverty level will pay the same amount of $15 for Dr. Dynasaur, even if one family has one kid and the other family has five kids.

Using 2013 federal poverty guidelines, VTDigger broke down what families of different sizes, earning different incomes, would pay for Dr. Dynasaur coverage. These are estimates because the guidelines will change in 2014.

Cost-sharing

State and federal cost-sharing subsidies can only be used with silver level plans. These subsidies are used to cap the amounts that Vermonters are liable for paying in health care costs.

This effectively reduces deductibles and out-of-pocket limits.

Unlike the premium subsidies, the cost-sharing subsidies are not reconciled at the end of the year. This means that if a Vermonter’s income rises, he or she will not be penalized for receiving this subsidy.

The cost-sharing subsidies are available to Vermonters earning up to 300 percent of the federal poverty level. That translates into $34,470 annually for an individual and $70,650 for a family of four.

Take, for example, a Vermonter earning $20,682 a year, or 180 percent of the federal poverty level. With cost-sharing subsidies, this Vermonter’s medical deductible for a standard silver plan would be capped at $750, and his or her out-of-pocket limit for medical expenses would be capped at $1,250. Without subsidies, a silver standard plan from Blue Cross would have a medical deductible of $1,900 and a medical out-of-pocket maximum of $5,100. The out-of-pocket maximum is the limit that a person would be liable for paying in health care costs in a year, and it doesn’t include the cost of premiums.

To see how cost-sharing subsidies would cap costs for different plans, click here.

Premium scenarios

Vermont is one of a few states in the country that is providing a premium subsidy in addition to the federal one.

The federal subsidies are used to cap Vermonters’ premiums at a percentage of their overall income.

The federal subsidies apply to Vermonters earning 138 to 400 percent of the federal poverty level. Using 2013 federal poverty guidelines, premium subsidies would be available to individuals earning up to $46,000 annually and to $94,200 for a family of four.

The Vermont subsidies apply to Vermonters earning 138 to 300 percent of the federal poverty level. What they do is lower the federal cap by 1.5 percent.

Here is how it works: Take a Vermonter earning $32,000 annually. The feds would cap this person’s premium at about 9 percent of his or her income, and the state would lower that to about 7.5 percent of his or her income.

The subsidies are tied to the second lowest cost silver plan: Blue Cross’s high deductible plan, carrying a monthly premium of $412.83. The federal subsidy would lower this Vermonter’s premium to about $236 a month. With the state subsidy, this Vermonter would pay $196 a month.

The monthly subsidy this Vermonter receives is $216.92, or the difference between $196 and $412.83. That is the difference between the monthly cost of the Blue Cross silver plan and the cost of a subsidized premium for the silver plan.

If this Vermonter decides he or she would like a plan with lower deductibles and out-of-pocket liability, he or she can apply this subsidy to that plan. A gold plan offered by MVP costs $513.83 a month. With the $216.92 monthly subsidy, the gold plan would cost this Vermonter $296.91 a month.

To calculate your subsidy, go to the state’s premium subsidy calculator or scroll down to VTDigger’s premium comparison.

Things to Keep in Mind with Premium Subsidies

The premium subsidy, as aforementioned, is not available to Vermonters who receive health insurance coverage from their employers.

Vermonters can choose to have their subsidies applied directly to their premiums or receive them at the end of the year. If a Vermonter receives the subsidy up front, it goes directly to the insurer and is based on an estimate of their annual income from the previous year. This subsidy will be reconciled at the end of the year based on his or her actual income.

Vermonters who see a rise in income could owe the federal government thousands of dollars when it comes time to pay taxes. Residents who see their income drop would be eligible for a larger tax return.

For Vermonters earning less than 200 percent of the federal poverty level, the most they would owe to the feds for a rise in income is $300 for an individual and $600 for a couple filing jointly. For residents earning between 200 and 300 percent of the federal poverty level, the most they would owe is $750 for an individual and $1,500 for a couple. Vermonters earning between 300 and 400 percent of the federal poverty line could owe as much as $1,250 for an individual and $2,500 for a couple.

Those Vermonters whose incomes exceed 400 percent of the poverty line — $45,960 for an individual and $94,200 for a couple — would owe the full subsidy to the federal government. To avoid this situation, Vermont Health Connect encourages Vermonters to report monthly changes of income.

Another important point to keep in mind for families is that if one spouse is offered a contribution from his or her employer, this does not necessarily prevent the other spouse from accessing subsidies, if an employer offers a contribution for a “self-only” plan.

If, however, an employer offers the same contribution, and makes family coverage available, this would prevent the other spouse who was not offered an employer contribution from accessing the subsidies. The family coverage is considered to be available regardless of whether the employer offers more of a contribution for families.

Premium subsidy scenarios

To show how the premium subsidies break down, VTDigger has created six premium subsidy scenarios for a single adult, two adults, a single parent with one child, a single parent with two children, two parents with one child, and two parents with two children.

VTDigger has created six interactive graphs for these scenarios. To choose a graphs below, click on the tab with your household makeup. VTDigger acknowledges that many families fall outside of these parameters. The graphs are meant for educational value as much as for personal use, and Vermonters wanting to calculate their estimated subsidy can do so using the state calculator.

To use the interactive graphs for each scenario below, find your household’s annual income on the horizontal axis. Move your cursor to the graphed line, and a window with your ballpark subsidy will appear.

If your income is below the lowest income on the graph, it is likely you are eligible for Medicaid. If your household income is above the income highest income charted, it is likely that you are not eligible for subsidies.

The graphs below are based on VTDigger calculations from data the administration and the Joint Fiscal Office have used to run subsidy scenarios. VTDigger used 2013 federal poverty lines, and the below graphs are meant to provide Vermonters with an idea of how the subsidies are calculated and a ballpark estimate of what premium subsidies they are eligible for.