Editor’s note: This commentary is by John Pelletier, who is director of the Center for Financial Literacy at Champlain College.

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness…”

from A Tale of Two Cities by Charles Dickens

In June 2019, the Pew Charitable Trusts issued their annual report on state public worker retirement plans. The report indicated that, as of 2017, Vermont’s funded ratio (the percent of plan accrued assets relative to the plan’s current accrued liability) was 64.3%, meaning that Vermont’s funding of its state pension plans was basically in the bottom third of all states in the country. The funded ratio lets Vermonters know if our savings are on track to pay the pension promises made. This report is telling Vermont that we have saved less than two-thirds of what should have been saved so far to meet this important obligation.

Surprisingly, our neighbor Maine had a funded ratio of 81.9% and was nearly in the top quartile of all states in the nation. This was a curious result, since Maine suffers from the same economic and demographic issues as Vermont. Both have old and stagnant populations, low economic growth and flat or declining workforces. How can Maine suffer from the same problems as Vermont and yet have dramatically more secure pension funds for its state employees and teachers?

Effective July 1, 2008, Vermont required that our state employees’ and teachers’ pension plans amortize their unfunded liabilities over a 30-year period. Basically, the Legislature required that the plans be fully funded on an amortized basis by the end of the 2038 fiscal year. It’s a bit like a mortgage on a home, except that this is not a fixed mortgage. Vermont’s payments from the general fund into these plans keeps rising.

So how has Vermont’s and Maine’s pension plans performed since the start of this legislatively mandated 30-year mortgage? Remember, this is when Vermont “fully funded” its pension obligations each and every year. Below is a summary of the funded ratio data from fiscal years 2009 to 2018. As you can see, in 2009 Vermont plans, in the aggregate, were doing better than Maine’s plans and yet by 2018 Vermont was far behind Maine:

A key driver to the success of any pension plan is the plan’s assumed rates of return on pension investment assets. When Vermont’s pension plans do not achieve this assumed rate of return, the difference must ultimately be made up by the taxpayers and reduces the tax dollars available for other state funded priorities. Being conservative (having a lower and realistic rate) is the prudent thing to do for pension participants, retirees and taxpayers.

As you can see below, Maine greatly increased the security and stability of its pension plans over these 10 years primarily by using realistic assumed rates of return and by having slightly better market value investment returns on the plans’ assets (however, Maine’s market returns, like Vermont’s were below Vermont’s pension plans’ peer group median return over this decade).

This makes sense, one would expect pension plan funded ratios to materially improve during a decade that is in the midst of both the longest bull market and economic recovery in U.S. history. But for some reason this did not happen in Vermont. Why?

Pension plans are only as good as their investment results and plan assumptions. Key assumptions relate to the plan participants’ actions as well as investment and economic results (e.g. assumed rate of investment return, when participants will retire, life expectancies of retirees, payroll increases of participants, cost-of-living adjustments for retirees, inflation rates, etc.).

Unfortunately, some of Vermont’s pension funds’ assumptions were overly optimistic and the actual investment performance of the pension portfolios was subpar over this period. In fact, the teachers’ and state employees’ plans over this decade (FY 2009 to FY 2018) underperformed 83% and 78% of their public pension peers, respectively, according to Sept. 25, 2018, reports given to the plans’ trustees. In August 2019 the Institute for Pension Fund Integrity issued a report that identified Vermont’s pension plans as being in the “Top 10 Worst Performing Pension Funds” in the country (looking at 10-year rates of return from 2013 to 2017).

Perhaps the biggest detractor over the last decade was the use of overly optimistic assumed rates of return. Particularly problematic was the use of “select-and-ultimate” rates of return from 2012-2015 (see footnote in chart above for how this system works). This method was used by Vermont (and some other states like Minnesota and Alabama) to materially reduce the payments required by the general fund to the pension funds in most of the years it was used.

The use of this unrealistic system over four years appears to be directly responsible for about 10% of the pension funds’ unfunded liability. The state’s actuary could be asked for a precise accounting — basically how much damage was done by moving from a flat 8.25% assumed rate of return to the select-and-ultimate system with Ponzi-like long-term return expectations.

Here is how the select-and-ultimate system reduced the amount of money the general fund had to put into the pension plans. In 2011, using an assumed rate of return of 8.25% the plans assets were expected to grow by a total $229 million, and if the plans had a lower investment return the general fund had to make up the difference. That did not occur because the plans investment returns that year exceeded 9% and no additional funding from the general fund was required that year.

In 2012, when the total pension plan assets were 9% larger than in the prior year, using the select-and-ultimate assume rate of return system, the plan assets needed to grow by only $187 million, much less than the prior year (an 18% reduction from the prior year). How is this possible? Well the select-and-ultimate systems pretends that a 6.25% return in 2012 is the same as getting an 8.4% average annual return until 2038 (27 years). Coincidentally and conveniently, both pension plans just met or exceeded this new assumed rate of return in 2012 — so no additional funding was needed from the general fund again that year.

If the old 8.25% assumed rate of return had remained in place, the plans would have been required to have investment returns of $234 million. Ultimately this actuary change saved the general fund $56 million in expenses in 2012. Similar general fund savings were also obtained in 2013 ($45 million) and 2015 ($56 million) using this method, but not in 2014 given the plans strong investment returns that year of over 8.25%.

Why was this done? Perhaps to protect politicians in Montpelier from making tough and painful choices? It is likely that a total of nearly $160 million in additional spending cuts or tax increases (or a combination of both) were avoided by using this clever actuary maneuver, once it was approved by the plan fiduciaries/trustees. Thankfully this practice ended in 2016, but not before pension members, retirees and taxpayers were harmed.

Assuming the very optimistic 8.25% assumed rate of return was retained in 2012 to 2015 (instead of the incredibly optimistic select-and-ultimate system) the general fund would have contributed an additional $157 million into these pension plans and with future investment returns, these additional plan contributions should have been worth about $241 million on June 30, 2019.

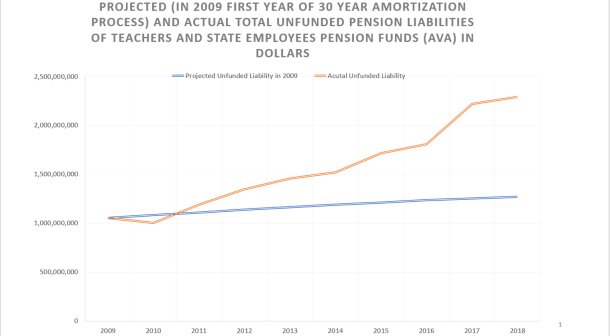

In 2009, Vermont’s state employees’ and teachers’ pension funds’ actuary predicted the size of Vermont’s unfunded pension liabilities each year until 2038 — the end of the state’s 30-year pension mortgage. They predicted that the unfunded liabilities of these pension funds would be, in the aggregate, $1.272 billion in 2018. The actual number in 2018 was $2.293 billion. We are one-third of the way through Vermont’s 30-year mortgage and the amount owed is now more than 80 percent higher than originally projected.

This was not caused by the Dean and Douglas administrations but primarily due to poor investment performance and the use of unrealistic pension assumptions since 2009. Twenty-two percent of this $1.021 billion increase in unfunded pension liability is directly attributable just to the single decision to move to the select-and-ultimate return method from 2012 to 2015. During the 14 years of significant underfunding in the Dean and Douglas years (when funding from the general fund was less than 90% of what was needed in the years 1991-2000 and 2003-2006) the total amount of underfunding equaled $160 million. That amount is nearly identical to the underfunding during the four-year period (2012-2015) when the select-and-ultimate rate method was used by the pension plans rather than the very optimistic assumed rate of return of 8.25%.

High unrealistic assumed rates of return results in lower payments each year from the general fund and ultimately higher unfunded liabilities in the future. For example, a 1% reduction in the current assumed rate of return (from 7.5% to 6.5%) of Vermont’s teachers’ and state employees’ plans would require an increased payment of $30 million a year into these plans from the general fund or from investment returns.

With 19 years left to our 30-year amortization, such a reduction would require $570 million in additional payments (or investment gains) into the plans and Vermont would be certain that it would have $1.234 billion in additional assets in the pension funds in 2038. If policymakers and plan trustees want to protect plan members and retirees they should embrace lower, conservative and realistic assumed rates of return. But such a policy will reduce funds available for Montpelier to spend on other existing or newly created programs.

At Champlain College’s Center for Financial Literacy, I have had the good fortune to work closely with more than 300 Vermont educators, helping them bring personal finance education into their classrooms. Each and every one of them is a hero in my eyes, deserving our respect and support. They also deserve the retirement benefits they have been promised. The teacher’s pension funded ratio should not be at a shockingly low 55%. To be protected in retirement, our educators must have a pension fund with at least average investment returns (relative to peers) and a realistic assumed rate of return. Over the last decade, both have been lacking from Vermont’s pension plans.

Vermont has followed Maine with regard to school consolidations (Act 46) and proficiency based learning (although a few months ago Maine changed its mind and outlawed proficiency based diplomas). Many believe that following Maine in these policy areas was a mistake. But it would not be a mistake to follow Maine’s wise example with regard to managing its state pension plans with more realistic pension plan assumptions and better investment returns on pension fund assets. Surely the pension plan members, existing plan retirees and Vermont taxpayers would agree that looking more like Maine from a pension perspective would be quite beneficial.