Editor’s note: This commentary is by Scott Thompson, a 27-year veteran of the U.S. Foreign Service, who now represents Calais on the U-32 school board.

[W]e have an education tax problem distinct from school spending. Contrary to what many believe, we cannot solve it by cutting school spending. Vermont has developed beyond the point where taxing property to pay for education can be rational, fair, or prudent. Personal income appears the best alternative tax base.

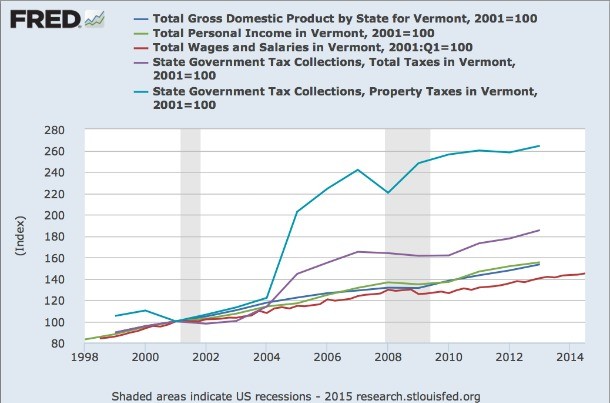

The graph shows relative changes in several broad measures touching on the question of education finance, indexed to 2001 levels. What jumps out most noticeably is the state’s property tax collections (light blue), nearly all of which is the education tax. This amount more than doubled, far outpacing every other metric.

Thanks to research done by Public Assets Institute and others, we know that total education spending has been highly stable as a percentage of the state’s economy since the 1990s. The dark blue line of Vermont’s total gross domestic product can therefore serve as a close approximation of the relative change in total school spending over the same period.

These two tracks — light blue for education tax, dark blue for school spending — differ markedly.

The big jump in state property tax appears to have jolted total state taxes (purple line) above the natural growth trend in our economy (dark blue line again). In other words, the education property tax is a major culprit in our perception of an “affordability problem.” The drooping trend line in wages and salaries (red line) depicts what many working Vermonters have been feeling for years: the sense of falling slowly, inexorably behind.

Resolving the enigma of the fever chart,/h4>

One might explain the spike in state property tax by the effects of implementing Act 68 in fiscal year 2005. Or by the state’s declining share of General Fund contributions to the Education Fund. Or by the result of piling the amounts subtracted via current use and income sensitivity back onto the correspondingly narrowed property tax base.

One might then dust off one’s hands, point out that the state property tax has recently resumed a trajectory more or less parallel to the state’s economy, and proclaim a New Normal.

But why settle for a Worse Normal? Deviant numbers call for a closer look.

Is there a problem with Acts 60 and 68? — Emphatically not with their core idea, which marks a genuine advance in the practice of democracy: local decisions on school budgets, statewide mobilization of resources to fund them, and mechanisms to adjust voters’ taxes equitably in line with the budgets they approve.

The state tax on non-residential property likewise seems to work roughly as intended.

But the homestead component of Vermont’s education property tax is another matter. It fails to carry out the intent of Acts 60/68 in any number of ways:

Revenue stream piracy — There is no inherent logic in taxing property to pay for schools. Under the old system, towns did it because they had no other option. The state, however, has multiple options. By assuming control of the education property tax and then letting it inflate to its actual dimensions, the state squeezes towns’ ability to fund local government operations.

Self-contradiction — The Common Level of Appraisal is a rich source of paradox. From the point of view of the state, what could be more fair than for each property owner to pay tax on the fair market value of his or her property? From the point of view of the taxpayer, what could be more unfair than to have to pay what amounts to a capital gains surcharge, based on the gains of a few who don’t have to pay it (because they sold their property), and imposed on the many who never received any gains?

The roughly 6 percent of gross state product that we spend each year is just what we should be spending in order to support a “world-class education system for all Vermont children.”

Arbitrariness — The Common Level of Appraisal is supposed to be a technical adjustment. Yet it often vies with the state-set rate for the dubious distinction of determining most of a town’s education tax increase. The more tightly school boards are able to control their budgets, the more outsized such external effects become. Short of neutron bomb-scale cuts, it is often impossible to blunt their impact, let alone zero them out, via changes to the school budget.

Broken feedback loop — When the change in a town’s tax burden has so little to do with the local school budget, the budget vote no longer sends a clear signal. If a school budget is voted down, was it the budget or the tax increase that voters opposed? No one can say for sure from the vote alone.

Instability — Towns can flourish with high property tax rates, though it helps greatly if rates are predictable enough over time to be factored into property values. The Common Level of Appraisal unfortunately tends to destabilize tax rates from year to year. Its façade of mathematical respectability belies an unscientific methodology of non-random sampling, which exposes it to the swings in fortune of local real estate markets.

Healthy numerator, sickly denominator

There is a silver lining. Having figured out how little they can influence taxes, school boards are freed to focus instead on what benefits students in their schools. And taxpayers, though put through the wringer year after year, continue year after year to reaffirm their commitment to providing the resources necessary for educational excellence.

In terms of the total amount we spend on education, those who argue that there is no crisis appear to be correct. The roughly 6 percent of gross state product that we spend each year is just what we should be spending in order to support a “world-class education system for all Vermont children.” Finland, the Vermont of Europe, perennial world chart topper, spends about 7 percent of its gross domestic product on education.

We are spending what we should. The problem is, we are not getting out of it all that we could. Our education spending problem is a problem of efficiency, not of absolute numbers. This problem is rooted in the denominator: falling enrollment, the result of Vermont’s bottom-scraping fertility rate. Social ills, administrative rigidities, lack of incentives, and many other factors aggravate it.

Although efficiency is the goal, there may be smarter ways to get there than by lopping off a big chunk of our educational capacity. We have a child welfare system that struggles to fulfill its mission. We have a Reach Up social welfare program that emphasizes adult education yet lies in this year’s budgetary cross-hairs. We have a state college system that is priced out of reach (and located out of reach) for many. Opportunities abound to weave these priorities together instead of letting them dangle separately, duplicating efforts here, leaving gaps there, and racking up costs everywhere. Our network of public schools under public oversight is a solid, well-distributed local platform to build such joint ventures upon. It is encouraging to see tentative steps in this direction already.

The great original capital of head, hand, and heart

We have the political will and social consensus to sustain the resource base for a world-class system. These blessings deserve a proper funding vehicle.

Not the homestead property tax. This belongs with the towns and school districts, where voters may exercise the right to tax themselves. State legislators, kindly give this tax back to the people, who can best use it.

The obvious alternative tax base for education is personal income from all sources (green line on the graph). It tracks gross state product most closely, and therefore most closely tracks total education spending.

Moreover, the logic missing from an education tax on property is wholly present in income. In addition to everything else, education is the formation of human capital — “the great original capital of head, hand, and heart,” in Ruskin’s sublime phrase. Capital yields income. A portion of present income thereby begets all future income in a virtuous cycle.

A well-run business invests retained earnings to generate future returns. A well-ordered society does much the same thing.

The can-do legislative ingenuity that gave us Acts 60 and 68 can surely structure an assessment on surplus personal income — that is, on personal income in excess of what households need in order to live. If each one of us who has surplus personal income pays our fair share, the state can maintain a stable and sustainable base rate, which may then be adjusted in line with taxpayers’ home district school budgets.

“The social purpose of skilled investment is to defeat the dark forces of time and ignorance that envelop our future.” What better investment for this purpose than education?

A note on the graph

The data series come from the U.S. Census Bureau (for state tax collections) and Bureau of Economic Analysis (for gross state product, personal income, and wages and salaries). They take visual shape thanks to the magnificent graphing tool “FRED,” created at the Federal Reserve Bank of St. Louis. The people who developed it deserve high praise for their contribution to civil society. For those of you unfamiliar with it, I urge you to check it out and put it to good use.