Editor’s note: This commentary is by Steve McKenzie, who is recently retired and lives in Waitsfield. It is an open letter to the sponsors of H.412, the carbon tax bill.

[T]o: Representatives Deen et al., sponsors of H.412, Establishment of Carbon Pollution Tax

As a concerned Vermont resident, voter and taxpayer, I have read your proposed bill in an effort to better understand the details vs. relying on the steady stream of opinions and interpretations (pro and con) for the contents and implications of the bill.

Professionally and personally, I am a strong proponent of efficiency in all areas: A core principle has been to never create or reward inefficiency. This requires careful and continual consideration and understanding of current and proposed processes.

A good process (in this case proposed legislation) must have a clear objective with well-defined supporting actions that are in direct alignment with the objective, and precise measurable metrics that clearly define progress and results. It is with this mindset that I have reviewed your bill and generated a series of initial comments and questions, below, and would welcome your feedback, and any clarifications of my interpretations, so I can better understand this proposal.

§ 8801. PURPOSE

The purposes of this chapter are to tax distributors of fossil fuels in order to reflect, in the price of these fuels, external costs of the carbon dioxide emitted from burning them and to reduce their use.

• What/where are the quantifiable objectives of this bill?

• What is the current baseline use of each fossil fuel type?

• Reduce the use of each by how much? By when? What are interim reduction goals?

• Without such metrics, a 1 percent reduction, at some undefined point, could be claimed a “success.”

• What are the current “external costs”?

• How do the proposed tax levels actually reflect the “external costs”? Presumably there was some calculation in defining the stated tax levels to support this purpose: please provide backup calculations.

• How/when will these external costs be affected/reduced by the tax?

• If the quantified purposes are achieved, where/what is the financial modeling of the net impact(s) in out years (other than the quantified dollar transfers)?

Overall, how can we clearly and objectively see the degree to which this bill has been directly effective (or not) in achieving the stated purpose?

§ 8807. EXEMPTIONS

The carbon pollution tax shall not apply to:

the sale of fuel to a company subject to the jurisdiction of the Public Service Board under 30 V.S.A. § 203(1) or (2), to be used at an in-state generation facility owned by the company for the manufacture of electricity to be used by the public;

This appears to be directly contradictory to the purpose of the bill. A generation plant that uses fossil fuel, or switches to fossil fuel, is not affected and/or has no incentive to move to any of the renewable energy sources listed on page 20, or burn more efficiently? Further, how does this exemption mesh with Vermont’s “90 percent renewable” objective?

§ 8810, page 8

(a)Each fiscal year, the revenues from the carbon pollution tax shall defray the Department’s actual costs in administering this chapter and the credits and rebates described in this section, up to a maximum of $300,000.00.

How will the actual cost to administer the tax be monitored? I do not believe an equivalent number of full time employees (three?) will be placed in charge of bill/tax administration to allow cost tracking. I assume incremental administration duties will be spread across other relative agencies. If yes, and actual incremental cost is greater than $300,000, the excess costs will show up unassociated and undefined in other budgets, providing no visibility to the actual incremental administrative costs of the bill.

§ 8810, page 9

(c) Each fiscal year, 10 percent of the revenues from the carbon pollution tax shall be allocated between the Home Weatherization Assistance Fund established under 33 V.S.A. § 2501 and the Vermont Energy Independence Fund established under 30 V.S.A. § 8015. Of this 10 percent, $8 million shall be deposited into the Home Weatherization Assistance Fund and the remainder shall be deposited into the Vermont Energy Independence Fund. However, if the amount to be allocated under this subsection is equal to or less than $8 million, then all of the amount shall be deposited into the Home Weatherization Assistance Fund.

Specifically, what will be the incremental and measurable benefit to Vermonters with this additional funding? What is/are the objectives of the additional funding (i.e., “the $8 million to the Home Weatherization Assistance Fund shall be used to assist an additional XX households)? What is the performance of the current Home Weatherization Assistance Fund and Vermont Energy Independence Fund? How many households are assisted for each dollar of current funding?

Without metrics, the actual effectiveness of the additional funding in supporting the bill’s purpose is impossible to determine. I don’t consider “We provided additional funding to Home Weatherization Assistance Fund and Vermont Energy Independence Fund” as a suitable definition of, or proof of, success.

SALES TAX ADJUSTMENTS

§ 8810, page 8

(b)Each fiscal year, 90 percent of the revenues from the carbon pollution tax shall be allocated to tax credits and rebates in accordance with this subsection. Of this 90 percent:

(1) The following specific dollar amounts shall be used to reduce the sales and use tax:

(A) for fiscal year 2018, $31.5 million;

(B) for fiscal year 2019, $48.6 million; and

(C) for fiscal years 2020 and following, $66.8 million

Page 15: 17 § 9771. IMPOSITION OF SALES TAX

(a) Except as otherwise provided in this chapter, there is imposed a tax on retail sales in this State. The rate of this tax shall be 5.5 percent during the first fiscal year in which this section is effective, decreasing by one-quarter percent on July 1 of each subsequent fiscal year until reaching five percent. The tax shall be paid by applying this rate to the sales price charged for but in no case shall any one transaction be taxed under more than one of the following: …

These two sections state the sales tax rate will be cut 0.5 percent in the first year, and 0.25 percent per year until reaching 5.0 percent, and specified annual transfer amount will come from carbon dioxide tax to offset the rate/revenue reductions beginning in year two, presumably to mitigate the net impact of the carbon dioxide tax to citizens.

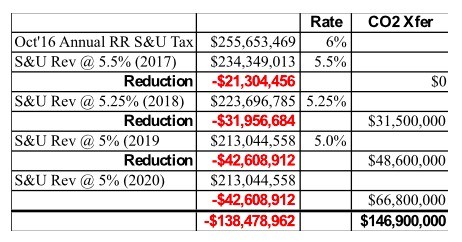

I used Oct ’16 year to date sales & use tax revenue figure from “Comparative Statement of Revenues” table, page 2, in the “Monthly Revenue Release” from Agency of Administration, dated Nov. 9, 2015, and created the following table to compare net effect. PLEASE NOTE: I have not made assumptions or adjustments for inflation, sales growth, etc., as commented below.

• Can you please provide your actual projections and assumptions?

• Where/how is the 2017/year one ($21 million) sales tax revenue loss made up in the state budget?

• In 2017/year one of the carbon dioxide tax, with no sales tax transfer/offset stated, I assume the equivalent carbon dioxide tax dollars will be distributed per other bill provisions?

• What are the assumptions made (gross sales growth, etc.) in the calculations that resulted in the defined transfer amounts in the bill?

• What are the projected annual deficits/surpluses vs. the current 6 percent rate?

• If the defined cuts in the sales tax rates result in sales tax revenue reductions greater than the specified transfer amounts, where is the difference to be made up in the general fund/budget? There should be clear language covering that possibility, and I would suggest any shortfall would come from an increase in the carbon dioxide transfer amount.

As a sales tax is by definition regressive and the income-sensitive rebate does not kick in until 2021, the carbon dioxide tax is therefore regressive until then, harming lower income earners more than higher earners.

This provision appears to be a key component in making this tax “sellable” to the average citizen: where are the “stops” to prevent the Legislature from enacting other fees/taxes, expanding application of the sales tax, etc., that would effectively negate any of the rebates and offsets provided under this bill?

§ 8811. PER EMPLOYEE CARBON POLLUTION TAX REBATE, page 10

(a) Each tax year, an employer shall be entitled to a per employee rebate for the number of its full-time equivalent employees, to be known as the per employee carbon pollution tax rebate. Each year, the Commissioner shall calculate the amount of this rebate per employee through dividing the amount of carbon tax revenue allocated to the rebate under subsection 8810(b) of this chapter by the number of FTEs.

(b) The Commissioner shall adopt rules to implement this section.

• While this is an easy administrative calculation, how is this fair/equitable to a given employer compared to actual taxes paid?

• For the purposes of proposed taxes paid, the amount per employee will vary significantly. An HVAC service business with 10 field technicians in vans will incur costs significantly greater than a CPA firm with 10 people.

• Is it your expectation that the full incremental costs of the tax will be passed along to consumers and therefore nature of a business is irrelevant?

• Line 8(b): Given the defined calculation, what additional rules are required?

• Are exemptions to be allowed?

• Will/could certain industries/businesses be excluded from qualifying for the rebate? At the discretion of the commissioner?

• It appears to me additional implementation guidelines must be defined in the bill for discussion/vote, not left to discretion of commissioner.

§ 5828d. CARBON POLLUTION TAX CREDIT AND LOW-INCOME TAX

12 REBATE, page 10

(a) A taxpayer shall be entitled to a refundable personal income tax credit against the tax imposed under section 5822 of this title, to be known as the carbon pollution tax credit. The Commissioner shall calculate this credit by apportioning the amount of carbon tax revenue allocated to the credit under subsection 8810(b) of this chapter to each taxpayer by filing status so that the amount of the credit is the same for each taxpayer filing as single, head of household, or married filing separately and, for married filing jointly, is double the amount assigned to the other statuses.

This is a very regressive approach: there is no differential made for income level.

The rebate is based solely on filing status until 2021, as defined under part b, page 11 of 30, line 1; b) For tax year 2021 and following, a taxpayer with federal adjusted gross income that is 200 percent or less of federal poverty level shall be entitled to a carbon pollution tax rebate.

Further, the flat credit calculation in no way reflects actual taxes paid by an individual, and taxpayers will be out of incremental tax dollars throughout a given year as this is apparently an annual credit (?).

As a sales tax is by definition regressive and the income-sensitive rebate does not kick in until 2021, the carbon dioxide tax is therefore regressive until then, harming lower income earners more than higher earners. Further, for those lower income earners who a) drive greater distances and/or b) have lower efficiency homes and/or c) have lower efficiency cars (and by definition of their lower income have less opportunity to reduce total energy usage), how will the net effect of higher net energy costs not impact them disproportionately to higher wage earners (who can absorb the additional cost and/or more readily address their total usage)? To what measurable degree will the increases to the Home Weatherization Assistance Fund and Vermont Energy Independence Fund funds address this issue for a given taxpayer?

Until 2021, this credit in no way reflects the actual incremental costs incurred by a given person, notably at lower income levels. A single person making $40,000 per year and commuting 75 miles per day will receive the same dollar rebate as a single person making $85,000 per year working from home as will a single elderly person living in a long-term care facility (i.e. not driving). Simply doubling the credit for married filing jointly couples will result in the same types of gross inequities in certain cases.

Can you please provide your forecasts and assumptions for the net personal impact under this bill for the following three examples (or any similar such scenarios you used in creation of the bill):

1. Single parent earning $40,000 per year, commuting 75 miles per day and 500 miles per month personal driving (approximately 24,000 miles per year) at 25 miles per gallon, and oil-based home heating at 1,000 gallons per year.

2. Married couple earning $100,000 per year, commuting 100 miles per day (combined) and 750 miles per month personal driving at 25 miles per gallon (approximately 33,500 miles per year), propane-based home heating at 1,500 gallons per year.

3. A contractor with 10 service vans, each driving 100 miles per day at 12 miles per gallon.

Overall, if the intent of these income rebates is to mitigate the overall impact of the carbon dioxide tax to an individual, how does that effectively incentivize an individual to reduce usage over time?

As I noted at the start, I am a strong proponent of promoting efficiency in all areas. Effectively doing so mandates clearly defined objectives, supporting processes and accurate metrics to define progress. Embarking on (or legislating) any efficiency effort without such details and backup is misguided at the very least. No such effort should be undertaken with a “we’ll figure out the details later” attitude. Without further understanding and clarification of this proposed legislation, I am extremely concerned that if enacted as currently written, there would be significant disruption and inefficiency with no definable or demonstrable results towards the stated purpose.

Thank you in advance for your feedback and guidance on this proposed legislation.