[V]ermont’s ski industry has outgrown the terms of decades-old leases of state land that were designed to help resorts grow and now result in lucrative deals for booming resorts, a state audit has found.

By most measures, the public-private partnership between resorts and the state is successful, but the lack of uniformity among leases creates a system that is difficult to control and creates extra cost for taxpayers, the report found.

Lease payments have declined over the past 20 years, when adjusted for inflation, the audit found. Ski resorts in the past half-century have diversified their revenue streams and those new sources are not captured in lease payments.

Hoffer on Tuesday called on the Legislature and administration to restart discussion on the leases and attempt to standardize the agreements. The leases give some ski resorts an advantage over others.

“I don’t think it’s unreasonable for someone to ask the question ‘are taxpayers getting a fair term?’” Hoffer said.

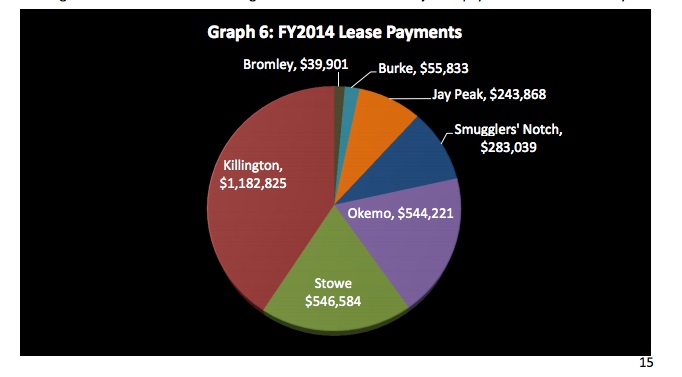

The auditor’s office in 2014 investigated the leases of the seven ski resorts that use public land: Bromley Mountain Resort, Burke Mountain Resort, Jay Peak Resort, Killington Resort, Okemo Mountain Resort, Smuggler’s Notch Resort and Stowe Mountain Resort.

The investigation aimed to evaluate the direct financial return to the public from the use of state land by the private businesses, many of which are now owned by out-of-state corporations.

The 50- to 100-year leases stem from agreements made in the mid-1900s. They govern about 8,500 acres of public land.

The earliest lease was initiated in 1942 with Bromley Mountain. The leases expire between 2032 and 2060.

The goal of the leases has been to develop and promote recreational sports in Vermont and to that end, the partnership have been successful, the auditor found.

“The intent was to help the industry develop and grow and that certainly has happened,” Hoffer said Tuesday in an interview.

However, the leases are outdated, he said. They were crafted when the resorts were locally owned, fledgling businesses that the state helped in order to boost tourism.

“It’s not as if they’re a start-up needing a helping hand,” Hoffer said.

Over the past 50 years, the resorts have transformed into booming, year-round attractions that include water parks, luxury hotels and condominiums, golf courses, biking trails and shops.

Over the past decade, development at the resorts has increased sales of goods and services, property values and revenue from excise taxes, the audit found.

At the same time, however, lease payments over the decade fell when adjusted for inflation.

Resorts pay the lease payments, whereas customers pay excise taxes.

For example, in the past decade, private property values at the seven resorts grew by almost 150 percent, according to the report, generating $5.3 million in property taxes.

In that same decade, inflation-adjusted sales of meals at the resorts grew by 40 percent, alcohol sales grew by 49 percent and rooms’ sales grew by 61 percent, the report said.

Over the same decade, the resorts’ inflation-adjusted lease payments to the state fell 14 percent, the audit found.

PILOT program

Since state lands are not subject to local property taxes, Vermont residents pay for land and facilities used by the ski areas through what are known as payments in lieu of taxes, or PILOTs. Those payments reduce the value of the lease revenues to the state, according to the report.

One of the most problematic inconsistencies is the variation in assigning title to properties on state land, which obstructs two towns’ ability to tax and gives some resorts a tax advantage because the development of property that belongs to the state is tax-exempt, the audit found.

One of the most problematic inconsistencies is the variation in assigning title to properties on state land, which obstructs two towns’ ability to tax and gives some resorts a tax advantage because the development of property that belongs to the state is tax-exempt, the audit found.

For example, in Killington, the town taxes property on state land that it should not, according to the report.

In the case of Smuggler’s Notch, the state PILOT appears to be skewed due to the inclusion of private property in the calculation and the fact that only one town receives payment for property located in two towns.

The leases also were written in non-standard terms and are inconsistent across criteria, such as lengths, indemnity clauses, remedies for breach of contract and audit provisions, the audit found.

Only four of the seven leases allow the state to audit the books of the resorts, and then only records concerning lease payments, the audit found.

All ski areas must file a financial report of their lease payments but the frequency of the reports varies among the leases.

All seven leases require the resorts to purchase public liability insurance to protect the state and its officials, according to the report. Outdated liability insurance language in the leases also pose a risk for the state, it found.

The Legislature is responsible for approving the leases, and the Agency of Natural Resources oversees the agreements.

The audit contains a chart showing fees collected by the state from resorts. In many cases the state collects 5 percent of gross lift ticket sales multiplied by the percentage of linear feet of lifts on state land, plus about 2.5 percent of gross receipts from restaurants, shops and warming shelters on state land.

The state also, in some cases, collects 3 percent of gross receipts from restaurants, sports shops and warming shelters built by the state on state land. In the case of Killington, the state collects $200 annually for the “employee lodge,” the report found.

The revenue from the leases goes to the Forest and Parks Revolving Fund, which funds the state’s parks division. The lease revenues have been a declining share of the parks’ budget, dropping from 41 percent to 32 percent of the division’s expenditures, the audit found.

The audit also compared property values with lease payments and found that property values grew at a rate of more than 13 times that of lease payments.

The resorts’ property values rose from $185.5 million in 2003 to $452.6 million in 2013, the report found.

The audit also found that lease payments at five resorts did not keep pace with the rise in ticket prices. Burke’s and Jay Peak’s lease payments grew faster than the change in lift-ticket prices.

Meanwhile, Vermont exempts ski lifts, snowmaking equipment and other resort machines from state education taxes. Tax bills show that $74.2 million in property was exempt from education taxes in 2013, according to the audit.

That exemption resulted in an estimated $1.1 million in foregone tax revenues for the resorts in 2013, according to the report. The total foregone amount for all resorts in the state would be higher.

Parker Riehle, president of the Vermont Ski Areas Association, said the leases have served the resorts and the state well. The resorts have no reason to renegotiate the leases until they expire, he said.

“The better that those sales are and the better that the ski rates are on state land the better that the lease payments are to the state,” Riehle said.

Michael Snyder, commissioner of the Department of Forests, Parks and Recreation, Tuesday said he agrees with the findings of the audit but the state’s hands are tied until the leases expire.

Snyder said his department supports the tradition of the lease program but is looking out for the state’s best environmental and economic interests.

“If there’s anything we can change we’re up for doing so,” Snyder said.