Editor’s note: This article is by Ayla Yersel and Timothy McQuiston of the Vermont Business Magazine.

About a third of Vermont small businesses have dropped their health insurance since the inception of Vermont Health Connect, according to a new survey, while very few companies have signed on. But it is very likely that nearly all those individuals employed in small businesses in Vermont have migrated to the state health insurance exchange.

Vermont Business Magazine and the Ethan Allen Institute conducted a statewide survey over the last several months asking whether small businesses offering health insurance to their employees in 2013 continued to do so in 2014. These businesses reported 50 or fewer employees and therefore were required to offer health insurance under Vermont Health Connect.

This bar graph indicates the number of businesses offering health insurance (blue) versus those that are not (red) in 2013 and 2014. All data, charts and graphs by Vermont Business Magazine.

The Vermont Business Magazine/Ethan Allen Institute Vermont Health Connect Exchange Survey was sent to 3,100 small businesses in Vermont. Nearly 500 employers responded.

For those companies who responded, some are not participating in the Vermont exchange because of cost and the complicated nature of the application process, which was exacerbated by the state’s website being unable to process small business applicants. Businesses who want to sign up for the exchange now are required to go directly through Blue Cross and MVP.

Of 456 total businesses that had made a decision about their health insurance coverage, 45.2 percent reported they will participate in the Vermont Health Care exchange. But only about 2 percent of all respondents reported that their businesses had not offered insurance in 2013, but planned to enroll in the exchange in 2014, and 36.5 percent of companies that offered health insurance coverage in 2013, dropped it in 2014.

“It’s clear from the survey numbers that there is still quite a bit of uncertainty surrounding the state’s health care policies,” said Robert Roper, president of the Ethan Allen Institute. “Where there is movement in the business community, it is overwhelmingly to stop offering insurance as a benefit and to send their employees into the currently dysfunctional Vermont Health Connect exchange, where these employees can claim Obamacare credits.”

“The Shumlin administration,” Roper said, “hopes to convert those credits to federal funding for Green Mountain Care (single payer) in 2017. Therefore, this divorcing of health insurance from employment is what the incentives in Act 48 were designed to bring about. Businesses who are concerned about their employees will have to consider whether unloading them into the exchange will be good for them, especially if the whole shaky scheme breaks down, leaving the employees with no insurance, no credits, and no Green Mountain Care.”

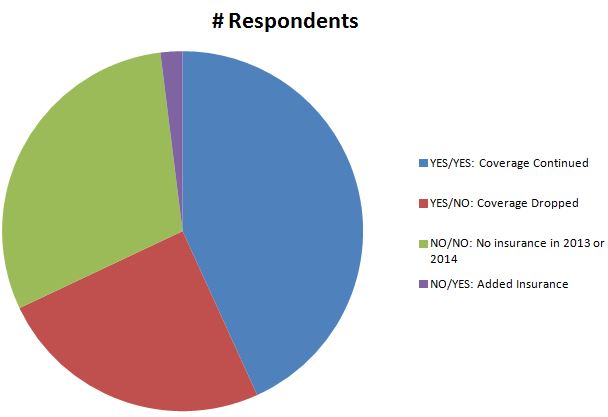

Survey Results

Company — Choice — Numer of respondents

YES/YES — Coverage Continued — 197

YES/NO — Coverage Dropped — 113

NO/NO — No insurance in 2013 or 2014 — 137

NO/YES — Added Insurance — 9

TOTAL — 456

(YES business offered insurance in 2013/YES business will participate in exchange in 2014) – 197

(YES business offered insurance in 2013/NO business will NOT participate in exchange in 2014) – 113

(NO business DID NOT offer insurance in 2013/NO business will NOT participate in exchange in 2014) – 137

(NO business DID NOT offer insurance in 2013/YES business will participate in exchange in 2014) – 9

According to the VBM/Ethan Allen survey, a majority of businesses entering the exchange in 2014 reported that they will offer the same premium coverage under the new health care plan. Of those companies who will continue to provide insurance, 77 reported that their employees would receive the same benefits in 2014 as in 2013, 11 reported they will offer greater coverage, and nine reported they will offer less coverage than in 2014.

Barbara Herrington of Greensea Systems Inc. said that her small business is unable to offer anything similar to the opportunities provided by the exchange.

“They can pay extra for better plans or enroll in cheaper plans, add dependents, etc.,” she said. “As a small company, we can’t offer anything similar via private insurance.”

“We believe the exchange provides the best opportunity for choice – we are giving employees the money and the opportunity to pick whatever plan they want,” she said.

Jim Grout of High 5 Adventure Learning Center said that the Affordable Care Act will allow his business to increase its contribution to 85-95 percent for the same cost of its old contribution.

“Our employees can use their savings to purchase a higher level plan with better coverage,” he said. “We save, they save, and get better coverage.”

Of all respondents, 54.8 percent reported that their businesses will not enter the exchange in 2014.

Of the 310 that offered their employees health insurance in 2013, 113 (36.5 percent) dropped health insurance coverage and therefore will not participate in the exchange in 2014.

This pie chart shows the ratio of businesses in Vermont offering health insurance in 2014 (purple and blue) to those that are not (green and red). The ratio of those offering insurance in 2013 is the sum of red and blue versus those who did not (green and purple).

Several factors played into a business’ reluctance to sign onto the exchange. Some respondents claimed the system was “disorganized,” and others said that the plans provided under the exchange offered less coverage for higher premiums.

Chris Abrams, owner of Real Good Tags Inc., said that it was in his company’s best interest not to enter VHC and thus require his employees to register as individuals.

“Only two of our employees plus myself opted for the insurance our company provided in 2013,” he said. “Both employees qualified for rate reductions under the VT Health Connect.”

Richard F Hamlin, PE, of Donald L. Hamlin Consulting Engineers, said that due to their experiences with the exchange, his firm decided not to provide health care for its employees for the first time since its founding.

“Our firm has provided health care for its employees since its inception in 1965,” he said. “This year, based on our experience with the exchange process, was the first year we considered ending that practice.”

He said that his staff wasted a significant amount of time trying to use the exchange, only to be told to deal directly with their carrier.

Douglas A. Priestley, president and treasurer of Lovejoy Tool Co. Inc., said that his company chose to enroll in the exchange, even though it will pay more in 2014 for less coverage.

“If we were to offer coverage in 2014 that is comparable to what we presently (2013) offer employees, it would increase our costs by 41 percent,” he said.

Priestley said that the attempt to enroll has caused “both confusion and frustration.”

“Many of our employees feel the state is favoring unemployed individuals by not offering more subsidies to the working,” he said. “Deductibles and out of pockets on most plans are too high. Some of the plans that don’t allow HSAs have higher deductibles than the ones that do.”

The comparison between 2013 and 2014 is not completely “apples to apples” in a couple of significant ways.

First, sole proprietors are no longer considered businesses, but rather individuals for the purposes of VHC.

“A lot of those who dropped it are sole proprietors, which I think skews those (VBM/Ethan Allen Survey) numbers,” said Betsy Bishop, president of the Vermont Chamber of Commerce. But no entity, private or public, knows exactly how many sole proprietors are involved.

The Vermont Chamber was the largest provider of VACE group coverage with 17,000 members insured through Blue Cross. The Affordable Care Act ended programs, such as the Chambers’ VACE plan, in which mostly small companies, including sole proprietors, could get group rates through the Chamber.

In Vermont they were all supposed to go into the Vermont Health Connect exchange. Because of the well-documented technical problems, most then had to sign up directly through an insurance carrier, but those members were not segregated by type, SP versus small business.

For Blue Cross, it had about 41,500 members at the end of 2013 in the small group plan (or before VHC kicked in) and about 35,000 in April 2014, said Kevin Goddard, vice president of external affairs at Blue Cross and Blue Shield of Vermont. The corresponding numbers for members in the individual plan is the reverse of that, he said, with 19,500 before and 24,000 after, which likely reflects the churning of businesses either dropping coverage or changing status from sole proprietor to individual.

Goddard said there are several thousand individuals “in the pipeline” from VHC, who still need processing.

“We’ve retained close to all the members we had before,” Goddard said. He said once all is said and done, Blue Cross membership in the small group could exceed previous numbers.

“It’s too early for us to have hard data on who is doing exactly what,” Goddard said.

M. Beatrice Grause is the president and chief executive officer of the Vermont Association of Hospitals and Health Systems. When Vermont Health Connect was first introduced, the hospitals feared that small businesses would drop coverage and employees would not pick it up, leaving a large pool of uninsured. They urged employers to retain health insurance coverage. Now that it appears there is no such pool and that there could be even more workers covered by the end of 2014 than in 2013, the hospitals, which Grause represents, seem more comfortable.

“It doesn’t matter how or where Vermonters purchase health insurance,” Grause said. “What’s important is working toward our shared goal of universal coverage.”

What also makes analysis so difficult is that a number of businesses have not yet had to make a choice of whether to offer health insurance or not, but neither the state nor the insurers know exactly how many.

For instance, businesses whose insurance annual date was not Jan. 1, could defer making a decision until that date arrived. As an example, Vermont Business Magazine will remain on its 2013 plan until Dec. 1, 2014. At that point VBM will have to decide whether to offer insurance or send its employees to the exchange as individuals.

Mark Larson, Department of Vermont Health Access Commissioner, said the various program changes, such as the change in status of sole proprietors; the varying annual dates for businesses; and the natural “churn” among policyholders (employment and marital status changes, etc.) “makes it very hard to track the migration of people from 2013 to 2014.”

Like Goddard, however, he sees the potential of more people being covered in 2014 than in 2013.

The Vermont Department of Financial Regulation, which regulates health insurance, will not release its survey of VHC participation until January 2015.

In an email, Larson expanded on small business participation in VHC, saying that it is difficult to compare 2013 and 2014 for a few reasons.

“Most associations stopped providing group insurance coverage (eg, VACE), which meant that those employers of small businesses began to offer Vermont Health Connect plans directly or decided to stop offering coverage,” he said.

“In any year, employees move from small to large employer, leave the state, or start taking advantage of a spouse’s health insurance plan,” he said.

“In 2014, employees had the additional option of choosing a Vermont Health Connect plan with financial help, if their employer-sponsored insurance was considered unaffordable,” he said.

“Employees are not tracked individually, so these shifts are difficult to quantify,” he said.

“In comparing data from January to May in previous years, one can see the small group market has decreased some, and the individual market has grown,” he said. “The market covering public programs, individual plans and small group plans has grown overall.”

“We expected to see some of these shifts based on the information above,” he said.

“Our goal is to ensure that Vermonters are covered by comprehensive health plans,” he said. “We will continue to work to ensure that Vermonters have the tools and support they need to access health insurance.”

For those businesses offering insurance in 2014, this pie chart indicates whether the level of coverage has remained the same (green), increased (blue) or decreased (red) from what they offered in 2013.

He said that the Department of Vermont Health Access appreciates the insurance carriers’ dedication to providing small group clients with the plans that they want.

“There are tax benefits associated with non-employer plans in the form of advanced premium tax credits and cost-sharing reductions that make health insurance more affordable,” he said. “This financial help is available to thousands of Vermonters based on their income.”

Back on the phone, Larson said, “We’ve taken our lumps, but I hope people see we’re making progress every day.”

There is currently no minimum employer contribution requirement in Vermont. To receive a federal small business tax credit, however, employers “must offer at least a 50 percent contribution to employee premiums,” according to the Vermont Health Connect website.

The federal government will begin penalizing U.S. citizens who do not have health insurance on their 2014 tax return, according to the VHC website

Depending on which is greater, the IRS will begin charging 1 percent of a household’s income, or $95 per adult and $47 per child. The cap for lower income families will be $285. For individuals, the penalty will cap off at roughly $4,500 to $5,000, according to the website.

Betsy Bishop and others advocate that the state’s first order of business is to fix the technical problems with the VHC website. Kevin Goddard wants to make sure that all individuals are able to sign up, now that businesses are able to go straight to the carriers.

Larson said the business part of the exchange website should be available sometime this summer, so businesses will have the option of signing up there, through a broker or directly through Blue Cross or MVP to make it as “convenient as possible.”

Bishop said the Chamber has supported and continues to support health care reform, but is concerned that Vermont businesses will continue to need to change course as the state heads toward single payer.

Her view is that most businesses have taken the path of least resistance and just found an exchange plan that most closely resembles the plan they had previously.

Some employers who dropped coverage clearly did so for the benefit of their employees, many of whom could take advantage of the federal tax credit. Larson also noted the benefit of the tax credit.

Bishop’s point is that Vermont is very close to universal health care now, with about 96 percent coverage, between the exchange, large group coverage, individual coverage (including those on the former Catamount plan), Medicaid and Medicare.

She said businesses will face another change in 2016 when the 50-100 employee group must get onto VHC and then another one in 2017, when the “all in” single payer plan is supposed to be enacted.

She agrees with the need and has supported health care reform. She and the Chamber are “laser focused” now on cost containment and how the new system will be financed.

Right now, businesses and their employees fund the system through premiums. In 2017 that will transition to some sort of tax system, which must raise about $2 billion. Perhaps, she said, the new system will be enacted incrementally.

“I think businesses need to prepare themselves for the next three years of a changing landscape in health care benefits,” Bishop said.

VBM/Ethan Allen Data

As the results show, 63.5 percent of those who offered insurance in 2013 will continue to do so in 2014, while nearly all of those companies who did not in 2013, will not in 2014 (93.8 percent).

All told, 45.2 percent of all businesses in the VBM/Ethan Allen survey will participate in Vermont Health Connect this year, nearly identical to the percentage of all Vermont companies which offered insurance in 2013 (47 percent, according to VHC).

The original VHC plan was that businesses, like individuals, would have to sign up for health insurance through the VHC website starting Oct. 1, 2013.

Because of significant technical problems with the website, Gov. Shumlin made the determination in late 2013 that businesses who chose to offer insurance in 2014 would be allowed to go directly through the insurer, either Blue Cross and Blue Shield of Vermont or MVP Health Care, the only two insurers offering plans to the small group market (50 or fewer employees) in Vermont.

Because the state wanted to focus on making sure individuals were able to sign up through the VHC website, the governor decided to allow businesses to go through BCBS or MVP directly again in 2015.

The assessment for a business which chooses not to offer insurance remains at $40 per employee per month until 2016.

Background from the Vermont Health Connect website

For the 47 percent of Vermont small businesses that offer insurance, the keep-drop question is a critical one.

A village market, say, staffed by lower- and middle-income employees (up to 400 percent of federal poverty level, or household income of $94,200 for a family of four) might consider dropping coverage in order to allow the employees to take advantage of federal tax credits. A law firm with high-income partners, on the other hand, might decide to continue their employer-sponsored insurance.

Employees in most Vermont households that use Vermont Health Connect (those with incomes up to 400 percent of the federal poverty level or $94,200 for a family of four) will be eligible for premium tax credits and/or cost-sharing subsidies to help pay for out-of-pocket costs. These two forms of financial assistance are not available to Vermonters in employer-sponsored plans.